The Red Sea shipping crisis revealed how heavily the global economy depends on a handful of maritime trade routes.

Most people rarely think about how the global economy actually moves.

A shirt stitched in Bangladesh can appear in a store in Europe just weeks later. A car assembled in Germany may contain components that have already crossed multiple continents. Even fresh produce often travels farther than most people do in a year before ending up on supermarket shelves.

For years, many businesses treated global shipping as a certainty. Businesses treated shipping as something that would work automatically, much like a light turning on when they flipped a switch.

For many companies, shipping became an afterthought.

Companies built inventory plans, delivery schedules, and customer commitments around the assumption that goods would arrive more or less on time.

That confidence began to unravel in late 2023. The disruption quickly spread beyond the Red Sea. The disruption affected Mumbai warehouses, Chennai ports, and relocation firms handling moves between India and the Gulf.

The Red Sea crisis became the biggest disruption to global shipping since COVID-19 after Houthi attacks targeted commercial vessels.

The Red Sea shipping crisis quickly evolved into a global logistics challenge.

Higher shipping costs, longer transit times, and missed deliveries quickly became major challenges across the logistics industry.

Understanding the Red Sea shipping crisis matters because it exposed weaknesses that many businesses did not realise existed.

The effects of the crisis will likely shape logistics planning long after conditions in the Red Sea stabilize.

Red Sea Shipping Crisis: Background and Context

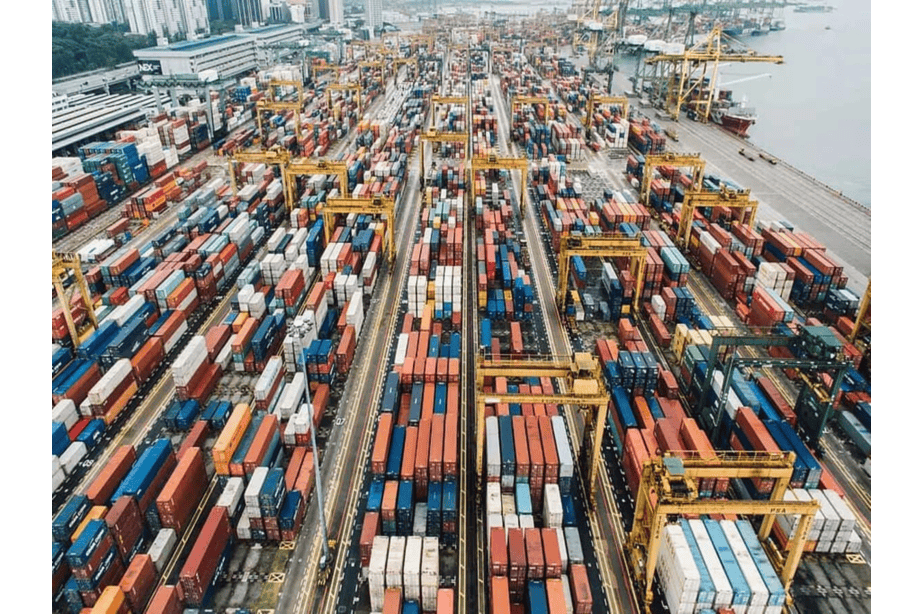

The Red Sea sits at the center of one of the world’s most important shipping routes.

It is the gateway to the Suez Canal, and through it flows approximately 12 percent of all world trade and nearly 30 percent of global container traffic, according to UNCTAD.

By linking the Mediterranean and the Red Sea, the canal provides the fastest sea route between Europe and Asia.

Without the canal, shipping companies reroute vessels around the Cape of Good Hope at the southern tip of Africa, adding thousands of miles and often several extra weeks to every voyage.

For India, the corridor carried particular strategic weight.

Approximately 65 percent of India’s crude oil imports, valued at around $105 billion in FY2023, passed through the Suez Canal, according to reporting by the Financial Times.

For exporters and importers operating through ports such as Mumbai, Chennai, Nhava Sheva, Mundra, and Cochin, the route offered one of the most efficient ways to reach European and Gulf markets.

Freight forwarders, warehouse operators, and relocation companies across India came to rely on the corridor’s reliability when planning shipments, quoting clients, and managing delivery expectations.

For years, businesses treated the route as dependable and planned accordingly.

Few expected the Red Sea shipping crisis to create problems across supply chains thousands of miles away.

Before the Red Sea Shipping Crisis

Before the attacks began, the global shipping industry was recovering carefully from the pandemic years.

Freight rates had stabilized. Port congestion had eased. Container availability had improved. Many in the industry believed the worst was behind them.

By 2023, traffic through the Suez Canal had reached record levels.

In FY2022/2023, the canal generated a historic high of $10.25 billion in revenues, according to the Suez Canal Authority.

More than 26,000 vessels transited the waterway that year. For shipping lines operating between Asia and Europe, the Suez route remained the quickest and most economical option.

A container vessel departing from a major Indian port for Rotterdam via the Suez Canal completed the journey in roughly 20 to 25 days.

Businesses had designed lean supply chains around this reliability. Safety stock was minimized. Delivery windows were tightened. Freight forwarders could quote rates with reasonable confidence because major costs rarely changed overnight.

The system was highly efficient, but that efficiency came with a trade-off. There was very little room for disruption once something went wrong.

Timeline of Events

The crisis began on October 7, 2023, when Hamas launched its attack on Israel, triggering the Gaza conflict.

Within weeks, Yemen’s Houthi movement, backed by Iran, announced it would target vessels it deemed connected to Israel, the United States, or the United Kingdom transiting the Red Sea.

The first significant attack on a commercial vessel came in November 2023.

By December, the frequency and severity of attacks had escalated to the point where the major shipping lines started rerouting vessels away from the Red Sea.

MSC, Maersk, CMA CGM, and Hapag-Lloyd all suspended or sharply curtailed Red Sea transits. What started as a regional security threat quickly evolved into a global logistics crisis.

By January 2024, six of the ten largest container shipping companies had either significantly reduced or halted operations in the corridor entirely, according to industry reporting.

The disruption deepened quickly. In March, the IMF reported that trade through the Suez Canal had fallen by 50 percent during the first two months of the year compared with the same period in 2023.

Attacks on commercial shipping continued throughout 2024. By October, Houthi forces had launched more than 190 attacks on commercial vessels, according to the House of Commons Library.

The United States and United Kingdom launched retaliatory strikes on Houthi positions in Yemen in January 2024, but the attacks on shipping continued.

By the end of 2024, only 13,213 ships had passed through the Suez Canal, down from more than 26,000 a year earlier. The sharp decline underscored how the Red Sea shipping crisis had become one of the logistics industry’s most significant challenges.

What Caused the Red Sea Shipping Crisis?

The Houthi campaign against commercial shipping, which the group described as solidarity with Palestinians in Gaza, served as the immediate trigger for the crisis.

The attacks exposed a problem that had been building for years.

A large share of Asia-Europe trade had become dependent on a single route through the Red Sea, leaving shipping companies with few practical alternatives when security conditions worsened.

Ships entering the Red Sea from the south must pass through the Bab-el-Mandeb Strait, a narrow waterway that has long been considered one of the most vulnerable points in global shipping.

There is no comparable alternative route through the region. When the security situation there deteriorated, shipping companies had exactly one option: go the long way around Africa.

Over time, companies had streamlined their supply chains to reduce costs and inventory. The downside was that there was very little room to absorb a disruption on this scale.

How the Red Sea Shipping Crisis Disrupted Global Trade

The rerouting around Africa via the Cape of Good Hope added approximately 3,500 to 4,000 nautical miles to every Asia-Europe voyage.

Transit times extended by 10 to 15 days on average, according to data from Xeneta.

Fuel consumption per voyage increased by up to 40 percent, according to FreightAmigo’s 2025 logistics report.

As ships spent longer completing each round trip, effective global container capacity fell by an estimated 10 to 15 percent. What looked like a simple routing adjustment quickly strained global container capacity.

Rising Shipping Costs

Freight rates reacted almost immediately.

The Shanghai Containerised Freight Index averaged 149 percent higher in 2024 compared to 2023, according to published index data.

During the early months of the crisis, the cost of moving a 40-foot container from Shanghai to Europe surged by approximately 250 percent compared to pre-war levels.

War-risk insurance premiums, previously negligible at under 0.1 percent of vessel value, climbed to between 0.7 and 1 percent by mid-2025, according to industry analysis by AInvest, adding hundreds of thousands of dollars in additional cost per voyage.

Costs rose at nearly every stage of the journey, leaving carriers with little choice but to pass a portion of the increase on to customers.

Delays, Congestion, and Capacity Shortages

The proportion of container ships arriving on schedule fell from 60 percent globally in 2023 to around 50 percent throughout 2024, according to supply chain tracking data.

Port waiting times at major hubs including Rotterdam and Singapore swelled by 20 to 30 percent during peak disruption, according to UNCTAD’s Review of Maritime Transport 2025.

UNCTAD report expects global maritime trade growth to fall from 2.2 percent in 2024 to 0.5 percent in 2025 before rebounding to an average of 2 percent annually between 2026 and 2030.

Together, these figures show how quickly problems in one shipping corridor spread through the wider logistics system.

Countries Hit Hardest by the Red Sea Shipping Crisis

The Red Sea shipping crisis inflicted some of its most visible economic damage on Egypt.

Canal revenues fell from a record $10.25 billion in 2023 to about $4 billion in 2024, a loss of nearly $7 billion, according to Egyptian officials.

For Egypt, the decline meant losing billions from one of its most important sources of foreign currency.

India experienced the effects of the crisis across several sectors. India’s dependence on crude oil imports, exports, and international relocation services exposed several industries to the disruption.

According to Financial Times reporting, the disruption directly affected key export sectors, including petroleum products, cereals, and chemicals.

Indian shippers diverted services around the Cape of Good Hope, absorbing significantly higher costs.

Delays in Asian imports disrupted factories across Europe, particularly in industries that depended on tightly timed deliveries.

Automotive production was among the most visible casualties. Tesla and Volvo temporarily halted production in early 2024 because delayed shipments created component shortages.

For Chinese exporters, higher shipping costs and longer delivery times made it more difficult to compete on both price and reliability.

Some African ports along the Cape route benefited from increased ship traffic and refueling demand. Bunker fuel demand at Mauritius’ Port Louis doubled to 1 million metric tons in 2024, according to S&P Global data. At the same time, many African importers paid more for goods.

While the effects varied from country to country, some industries felt the disruption more acutely than others.

Industries Most Affected by the Red Sea Shipping Crisis

Automotive manufacturing was among the hardest-hit sectors. The sector’s just-in-time production model leaves almost no tolerance for component delays. Tesla and Volvo drew the most attention, but the disruption affected manufacturers across the industry.

Food supply chains experienced delays affecting products such as avocados, tea, and coffee, according to published reporting. Agriculture was also affected as shipments of fertilizers, seeds, and crop protection products faced delays.

Longer transit times created delivery and inventory challenges for consumer electronics companies that rely heavily on Asia-Europe trade.

Retail businesses planning seasonal inventory faced serious difficulty predicting arrival dates. Many responded by holding more inventory, despite higher warehousing costs.

The energy sector also faced price volatility as concerns grew around the Strait of Hormuz, a key oil transit route that carries roughly 8.8 million barrels per day according to the US Energy Information Administration.

What the Red Sea Shipping Crisis Means for Logistics Companies

For many logistics companies, the crisis became tangible when customers began asking questions that nobody could answer with confidence.

When would the shipment arrive?

Would the quoted rate still hold?

Was the cargo already at sea, or had it been rerouted?

The disruption highlighted how much global logistics depends on a few major trade routes. Freight forwarders revised schedules, while importers adjusted inventory plans as delays stretched into weeks. For many businesses, schedules that had been reliable for years suddenly became difficult to trust.

The impact was particularly visible in the relocation industry.

Household goods shipments move on the same vessels as commercial cargo.

When ships were diverted around the Cape of Good Hope, relocation providers faced the same problems as freight operators: fewer containers, longer transit times, and higher costs.

Companies managing moves between India and the Gulf had to adapt quickly. Customers still expected firm delivery dates, but shipping schedules were changing regularly, making planning far more difficult.

Companies with strong carrier relationships, alternative routing options, and clear communication with clients generally handled the disruption better than those relying on a single network or supplier.

The crisis also changed how many companies think about risk. Companies that had invested in contingency planning and operational resilience were often better positioned to manage disruptions.

For years, logistics planning focused heavily on efficiency. The events in the Red Sea showed that flexibility and resilience matter just as much.

Future Outlook for the Red Sea Shipping Crisis

Following the Gaza ceasefire in early 2025, tensions in the Red Sea began to ease, but shipping companies remained cautious about returning.

Maersk signaled plans to resume Suez Canal transits, while the Suez Canal Authority offered toll incentives to attract vessels back to the route.

However, a swift return carries its own risks.

Global container capacity grew 10 percent in 2024 to 31 million TEUs, with another 6 percent increase expected in 2025.

If ships return too quickly, Asia-Europe routes could face excess capacity and falling freight rates. Xeneta forecasts a potential 49 to 59 percent drop in spot rates from 2024 peak levels if rerouting reverses rapidly.

Whether companies make lasting changes to how they manage supply-chain risk remains to be seen.

Some European firms have already shifted sourcing closer to home, turning to countries such as Turkey and Morocco instead of Asia.

Others have invested in air freight and rail alternatives, while safety stock levels have risen across multiple sectors.

For India’s growing logistics and relocation industry, the crisis served as a major test. Firms that adapted their networks, diversified suppliers, and strengthened contingency planning built greater resilience against future disruptions.

Conclusion

The Red Sea shipping crisis did not create a new weakness in global trade. It simply exposed one that had been hiding in plain sight.

The disruption to Red Sea traffic created ripple effects across industries, from the finances of the Suez Canal Authority to relocation companies moving household goods between India and Dubai. While some businesses faced greater challenges than others, few escaped the crisis entirely.

Canal revenue fell from a record $10.3 billion in 2023 to about $4 billion in 2024, highlighting the economic impact of the crisis.

The crisis also served as a reminder that reliable trade depends on stable routes, functioning infrastructure, and confidence across the supply chain. When one of those elements breaks down, the effects rarely remain local.

The companies likely to emerge stronger are those that used the disruption to improve contingency planning, diversify networks, and strengthen customer communication.

For an industry built on timing, the Red Sea shipping crisis showed how a disruption in one narrow corridor can ripple across supply chains worldwide.