Global freight is undergoing a transformation, with multimodal logistics emerging as the foundation of resilient supply chains.

Geopolitical uncertainty, capacity constraints, and market volatility are reshaping how operators and forwarders approach transport strategy.

Those that have historically relied on a single mode are finding that flexibility, connectivity, and diversification are no longer optional, they are fundamental requirements for long-term competitiveness.

The conditions driving this shift are not temporary. Trade tensions, port closures, and geopolitical flash points have become permanent features of the logistics landscape. In that context, a multimodal network is not a strategic upgrade. It is the baseline for any operator that intends to remain competitive.

The Multimodal Logistics Market in Numbers

The numbers confirm what operators are already experiencing on the ground. From $52.3 billion in 2025, the global multimodal logistics market is forecast to nearly double to $90.8 billion by 2034, growing at a CAGR of 7.2%., as mentioned in the report.

Approximately 52% of international shipments already rely on two or more transport modes, and close to 44% of logistics operators report higher delivery reliability through multimodal integration.

These figures reflect a fundamental change in how serious freight businesses think about their networks.

The Cost of Depending on One Mode

In April 2026, freight company HLS Group reported 80 cancelled sailings from China as trade tensions between the United States and China intensified.

When the two countries temporarily paused planned tariff increases, shippers quickly moved to take advantage of the opportunity. Within weeks, container bookings surged by nearly 300%, overwhelming port operations and stretching carrier capacity almost overnight.

Assembly lines paused. Inventory buffers collapsed. Deliveries missed their windows. Operators who depended on a single mode of transport had nowhere to turn.

And this was not an isolated event.

Less than a year later, when conflict erupted around the Strait of Hormuz in early 2026, shipping traffic through the waterway collapsed by nearly 95% within the first three weeks, stranding around 200 compliant tankers in the Middle East Gulf and triggering what analysts described as the largest oil supply disruption in history.

Taken together, these events point to the same conclusion: single-mode operators face more than rising costs and delays during disruptions.

Without alternative routing options, they risk operational paralysis the moment their primary transport mode becomes constrained or unavailable.

What Each Mode Brings to the Network

Air, sea, road, and rail each serve a distinct role within a well-designed multimodal transport strategy. Understanding those roles, and their limitations, is the starting point for building a network that performs under pressure.

Air Freight: Speed at Premium

When a pharmaceutical shipment has a 48-hour viability window or a factory is waiting on a critical component to keep an assembly line running, air freight is not one option among several. It is the only option.

In 2026, IATA projects global air cargo volumes to grow 2.4%, reaching over 71.6 million tons, with Asia Pacific leading at 6% growth, driven by cross-border e-commerce and surging demand for AI-related hardware and semiconductor components.

Air freight typically runs six to ten times more expensive per kilogram than sea freight on comparable routes. For anything that is not urgent or high-value, building a logistics strategy around air freight is commercially unsustainable at scale.

It performs best deployed selectively, at the moments when speed justifies the premium, not as a default across the supply chain.

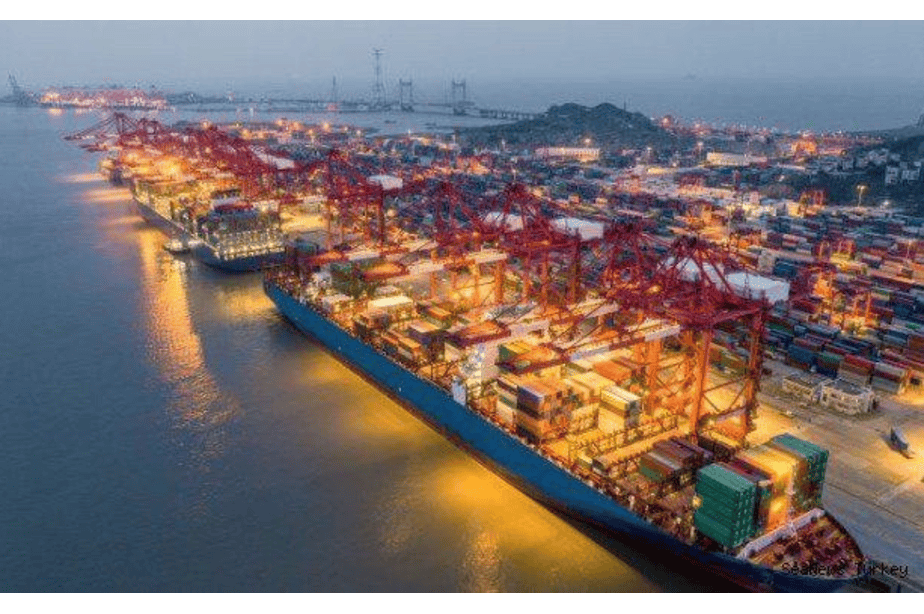

Sea Freight: Volume at Scale

More than 80% of global trade by volume travels by sea, according to UNCTAD. For large, non-urgent shipments crossing international borders, ocean freight remains the most cost-effective option available by a considerable margin.

Maritime trade volumes reached 12,292 million tons in 2023. Rates in 2026 have returned to near pre-pandemic levels on most major lanes, offering a more predictable cost environment than the previous three years.

That predictability should not be mistaken for stability. Houthi attacks on Red Sea shipping lanes, blank sailings, and carrier alliance restructuring have demonstrated repeatedly how quickly ocean freight markets shift.

Operators who rely exclusively on sea freight absorb that disruption risk entirely. Those who build it into a broader multimodal strategy retain the cost advantage while keeping the ability to reroute when the market moves against them.

Road Freight: First and Last Mile

No aircraft lands at a factory floor. No container vessel docks at a distribution centre.

Road freight is what gets cargo through the door when every other mode has done its job and that makes it the one link in the supply chain that cannot be cut.

Driver shortages across the United States and Europe have become one of the most persistent structural problems in global freight. Fuel costs swing without warning. Border delays eat into delivery windows that were already tight.

And yet road freight remains the backbone of domestic freight movement across North America, Europe, and South and Southeast Asia because nothing else replaces it where the supply chain meets the real world.

The operators who understand this do not try to minimise road freight. They deploy it precisely, at the first and last mile, and let rail and sea carry the weight on the long haul.

Rail Freight: The Sustainable Middle Ground

Rail does not compete with road on flexibility or air on speed.

What it offers instead is increasingly hard to find elsewhere in freight: predictability, scale, and a measurable emissions advantage at competitive cost.

Using rail for long-haul segments can cut carbon emissions by up to 75% compared to trucks and reduce shipping costs by 10 to 15% on all-road equivalent routes, according to the International Union of Railways.

The India-Middle East-Europe Economic Corridor, announced at the G20 Summit in 2023, places rail at the centre of a new overland freight route connecting Mumbai to European markets. China-Europe rail services now operate across more than 70 routes under the Belt and Road Initiative.

Rail depends on fixed infrastructure and always requires road freight at either end to complete the journey.

That is not a weakness, it is exactly how multimodal thinking is supposed to work. Rail handles the long haul efficiently. Road handles the endpoints. Together they outperform either mode operating alone.

Why no Single Mode is Enough

No single mode offers speed, cost-efficiency, flexibility, and sustainability at the same time.

Air freight cannot match sea freight on cost. Sea freight cannot match road on last-mile flexibility. Road cannot match rail on emissions or long-haul efficiency. Rail cannot match air on speed.

Each mode has a ceiling and that ceiling becomes a crisis the moment market conditions push freight up against it.

A multimodal logistics network routes freight through the right mode at the right leg of the journey and switches when any single mode becomes unavailable or too costly.

The One Ledger Thesis

The problem most operators face is not a lack of access to multiple transport modes. It is that they manage each mode in isolation.

Separate carriers, separate contracts, separate data systems, and separate communication chains produce fragmented freight: a supply chain where no single party has full visibility, and where a disruption at any one node cascades through the rest undetected.

The solution being adopted by the most competitive freight forwarding partnerships globally is what industry professionals are calling the one ledger approach.

This model consolidates every shipment leg into a single contractual framework, creates a single point of accountability, and enables real-time coordination through a unified data environment.

Here, the shipper does not manage a road carrier, an ocean carrier, and an air freight provider separately. One operator manages all three, with full visibility at every transfer point.

According to Matthew Castle, Global Vice President of Forwarding Products and Services at C.H. Robinson, speaking in Air Cargo Week in February 2026, “Our work focuses on building robust multimodal solutions that support shippers in navigating volatility and ensuring supply chain resilience.”

By integrating visibility, coordination, and routing across transport modes, the one ledger model keeps freight moving through disruptions instead of focusing solely on lowering costs.

The platforms making this possible are scaling quickly.

Digital freight forwarding reached $42.46 billion in 2025, growing at 18% a year. Over 70% of forwarders now run digital operations, processing 1.2 billion booking transactions in 2024 alone.

Route optimisation is the most adopted technology in the sector, with 51% of logistics companies using it and operators like DHL cutting delivery costs by 20%.

Air Cargo vs Sea Freight: Making the Right Call

One of the most consequential decisions in multimodal transport strategy is when to move freight between air and sea. Ocean freight rates have returned to near pre-pandemic levels, making sea freight attractive for non-urgent volumes.

For time-sensitive or high-value inventory, however, the cost differential becomes irrelevant the moment a port closes or a vessel is rerouted.

As iContainers noted in its Ocean Freight Market Forecast 2026, “Ocean freight will remain the most cost-effective option for large volumes, while air freight will continue to serve time-sensitive shipments despite higher costs. Resilience in 2026 will come from flexibility and informed decision-making.”

The operators who will perform best are not those who choose one mode as a standing policy. They are those who make the air-versus-sea decision at the shipment level, in real time, based on current data on rates, capacity, transit times, and disruption risk.

That capability comes from operating within a verified multimodal network, not from a single carrier relationship.

Why Verified Networks Win

Every structural challenge in global freight points to the same solution: network quality. The quality, reliability, and geographic depth of the freight forwarding partnerships an operator can access determines how well that operator performs when conditions change.

A Market Shifting Towards Multimodal Capacity

Fortune Business Insights forecasts that the global freight forwarding market will reach $536.51 billion by 2034, up from $336.61 billion in 2026, growing at a CAGR of 6.0%. The most significant competitive shift within that growth is toward multimodal capability.

Corporate buyers are demanding flexible transport options to navigate port delays, capacity shortages, and geopolitical uncertainty.

As new volumes emerge across Vietnam, India, Mexico, and the Middle East, forwarders leverage verified partner relationships to secure market share and expand their presence on these growing trade lanes.

Why Independent Multimodal Builds Fall Short

Building multimodal capability independently, carrier by carrier, country by country, mode by mode, is neither scalable nor practical for most operators.

Those that instead participate in verified multimodal networks capture disproportionate growth because they connect with vetted operators across all four modes, gain access to shared visibility infrastructure, and execute dynamic rerouting strategies that fragmented operators struggle to achieve.

How Movers Connect Powers Multimodal Networks

This is the gap that the Movers Connect platform addresses. By connecting operators, forwarders, and supply chain leaders within a verified network ecosystem, Movers Connect provides the infrastructure for genuine end-to-end logistics integration.

Participants gain access to vetted multimodal partners across air, sea, road, and rail, shared intelligence on route performance and disruption risk, and the collaborative framework that makes real-time freight decisions possible across borders and modes.

In an industry where 49% of shippers adopt multimodal logistics specifically to reduce congestion risk, and where nearly 35% of logistics firms report improved supply chain resilience through diversified transport modes, the value of that verified network is measurable, not theoretical.

The Road Ahead

Operators will shape the future of global freight by moving seamlessly across all four transport modes, making informed decisions at every leg of the journey, and using verified network partnerships to execute efficiently under any market condition.

Single-mode operators built strong businesses in a simpler era. That era has passed.

Ultimately, the operators who will lead the next decade of global logistics are those who have committed to multimodal transport strategy, invested in end-to-end logistics integration, and embedded themselves within verified freight forwarding partnerships that make global supply chain resilience a daily operational reality rather than an aspiration.

The network is the advantage. The operators who build it today will not just survive the next disruption, they will be the ones their clients call when everyone else cannot deliver.